Table of Contents

“PAY-OFF DEBT FIRST OR INVEST ?” The biggest question after receiving your monthly salary is how to spend it wisely. For those with debt, this is even more pressing. Should you pay off all your debts, loans and credit card bills first or should you start investing for the future?

Inflation is rising, jobs are unstable. Money is needed for every need, from children’s education to retirement. In such a situation people often find themselves confused about which step to take first for financial security.

Paying off debt reduces the interest burden, but not investing leaves your future plans incomplete. Striking a balance is the true wisdom. The question isn’t whether paying off debt or investing is better, but rather when to prioritize which based on your income, expenses, and goals.

Should you Pay-off Debt first or Invest for the future?

Debt and investment are two decisions that determine your current and future financial situation. Often, employed or middle-class individuals face a dilemma: should they pay off their debt first or should they save a little and start investing?

Should individuals with outstanding debt prioritize paying off their loans or investing?

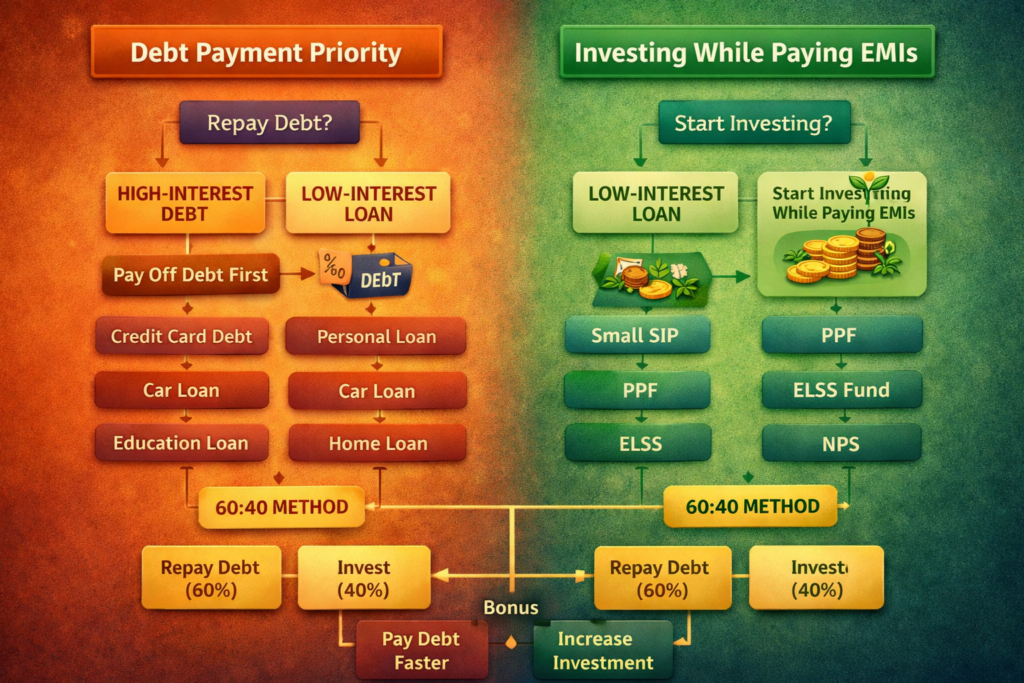

This depends on the type of debt you carry and the associated interest rate. If the interest rate on the debt is very high—such as with credit cards (30–40%) or personal loans (12–18%)—you should prioritize paying them off first. This is because the average return generated from investments is typically lower, falling within the 7–12% range. Consequently, continuing to pay interest on such high-cost debts for an extended period can prove financially detrimental. Conversely, if you hold “cheap” debt—such as a home loan with an interest rate of 7–9% that also qualifies for tax exemptions—you can simultaneously pursue investment opportunities alongside your loan repayment.

Which should be paid off first: a credit card, a personal loan, or a home loan?

You should prioritize paying off the debts that carry the highest interest rates first. Let’s understand this better through a graphic.

If I am currently paying EMIs, should I postpone investing?

If your EMIs consume a balanced portion of your monthly income—specifically, if they account for 30–40% of your earnings while still allowing for some savings—you should definitely start investing, even if it is with a small amount. This not only fosters financial discipline but also helps build a fund to cover future emergencies or major expenses. Through a Systematic Investment Plan (SIP), you can start investing with as little as ₹500 per month.

Is it possible to start investing with a small amount while simultaneously paying off debt?

Yes, investing does not always require a large lump sum to begin. You can start with as little as ₹500 or ₹1,000 per month through instruments like SIPs or Recurring Deposits (RDs).

- SIP (Systematic Investment Plan): Monthly investment in equity mutual funds.

- PPF (Public Provident Fund): A secure and tax-free investment option.

- NPS (National Pension Scheme): Useful for retirement planning.

How do I decide whether to prioritize paying off debt or investing?

You can make a simple comparison:

If the interest rate on your debt is higher than the potential returns from your investments, prioritize paying off the debt first. If the interest rate on your debt is lower than your potential investment returns, focus on investing.

Let’s understand this with an example. If you have a loan with a 14% interest rate and are earning a 10% return from mutual funds, paying off the loan first would be the right decision.

Can a home loan be carried for a longer duration compared to a personal loan?

A home loan is the only type of debt that offers tax exemptions. Exemptions are available on the principal amount under Section 80C and on the interest paid under Section 24B. Furthermore, interest rates on home loans are typically lower; therefore, there is no pressing need to repay them prematurely—unless, of course, your income is unstable.

How should one begin investing if they currently have outstanding debt?

You can start by considering the following options.

- Prioritize Before Investing

- Emergency Fund: Keep an amount equivalent to 6 months’ worth of expenses in savings accounts or Fixed Deposits (FDs).

- Health and Term Insurance: Essential prerequisites for any financial plan.

- SIPs in Mutual Funds: Gradually increase your investment amounts over time.

- Post Office Schemes: Safe and stable investment options.

Is it necessary to invest—even while in debt—specifically for the purpose of saving on taxes?

If your income falls within a taxable bracket, making investments under sections such as 80C, 80D, etc., becomes essential. However, this does not imply that you should neglect your outstanding debts. Allocate any funds remaining after making your mandatory tax-saving investments toward repaying your debts.

How can one balance debt repayment and investments when income is limited?

- Adopt the 60:40 formula: Use 60% of your available funds to repay debt and 40% to make investments.

- Create a budget at the very beginning of the month and cut down on non-essential expenses.

- Use any bonuses, incentives or tax refunds you receive to pay off additional installments on your debt.

- Set up an auto-deduction facility for your SIPs to ensure that your investment schedule remains uninterrupted.

Is there a specific formula for deciding between debt repayment and investment?

Yes, there is a simple rule for this.

- If you have debt with an interest rate higher than 10%, pay it off first.

- If you have debt with an interest rate lower than 7%, you can prioritize investing.

- If you have debts with interest rates between 7% and 10%, strike a balance between the two.

If one’s income is irregular, should they prioritize paying off debt or investing?

If you hold a job or run a business where your monthly income is inconsistent, the first priority is to build an emergency fund. Keep an amount equivalent to at least six months’ worth of expenses in a savings account or a Fixed Deposit (FD). This ensures that your EMIs and essential expenses can be met on time. If you have high-interest debts—such as personal loans or outstanding credit card balances—pay those off first. You should only begin investing once your emergency fund is fully established and you are able to pay your EMIs without any delays. In such a scenario, flexible investment options—such as Recurring Deposits (RDs)—are generally preferable to Systematic Investment Plans (SIPs).

Should one wait until all debts are cleared before investing, or can both activities proceed simultaneously?

Both can certainly proceed simultaneously; you simply need to determine the allocation ratio wisely. If your EMIs consume 30–40% of your income, you should begin investing with the remaining amount. By doing so, you are simultaneously reducing your debt burden on one hand, while building a financial corpus for your future needs on the other. Investment avenues such as SIPs, PPF, or NPS prove to be highly beneficial over the long term. Over time, this approach will lead to a reduction in your debt and a growth in your investments, thereby establishing financial security on both fronts.

Thank U